Car insurance is more than just a legal requirement; it’s a financial safety net that protects you from unforeseen events like accidents, theft, or natural disasters. In India, where road conditions can be unpredictable and traffic laws are often overlooked, having the right car insurance plan is crucial. But with numerous options available, how do you determine which car insurance plan offers the most value?

Key Takeaways

- Car insurance protects you financially from losses due to accidents, theft, or damage to your vehicle and others.

- There are two main types of car insurance plans: Third-Party Liability (mandatory and basic) and Comprehensive (broader coverage).

- Claim Settlement Ratio (CSR) is an important factor — a higher CSR means the insurer is more reliable in paying claims.

- A network of cashless garages helps you get your car repaired without upfront payments.

- Add-on covers like zero depreciation, engine protection, and roadside assistance can enhance your car insurance plan.

- Maintaining a No Claim Bonus (NCB) rewards you with premium discounts for claim-free years.

- Your premium depends on various factors like your car model, driving history, coverage type, and location.

- Always compare multiple car insurance plans based on coverage, cost, claim service, and customer reviews to find the best value.

- Car insurance is not just a legal requirement; it provides peace of mind and financial security on the road.

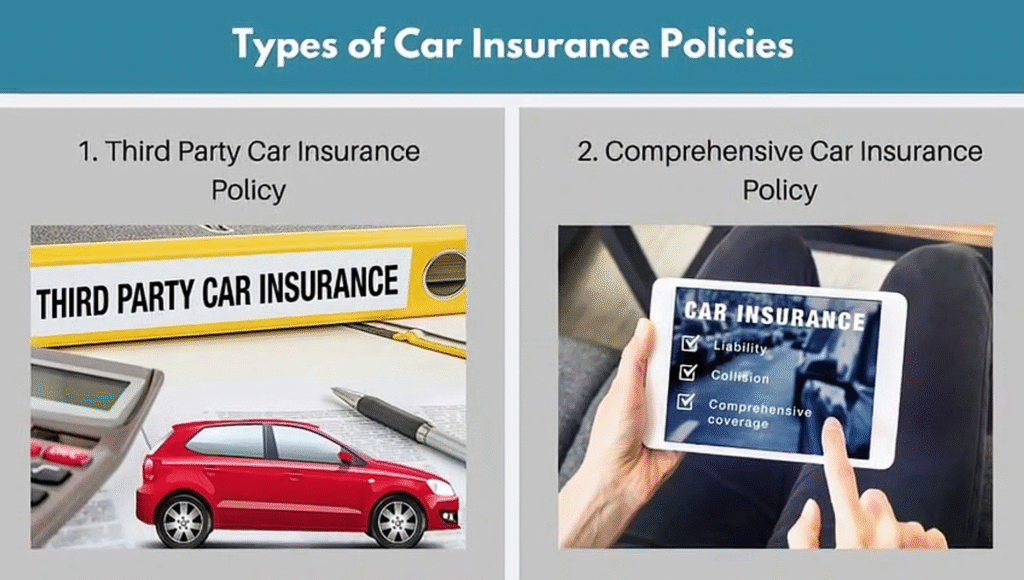

Understanding Car Insurance Plans

Before diving into the specifics, it’s essential to grasp the two primary types of car insurance plans available in India:

- Third-Party Liability Insurance: This is the most basic form of car insurance, covering damages to third parties involved in an accident where you’re at fault. It doesn’t cover damages to your own vehicle.

- Comprehensive Car Insurance: This plan offers broader coverage, including third-party liabilities and damages to your own vehicle due to accidents, theft, fire, or natural calamities.

For most car owners, a comprehensive car insurance plan provides the most value, as it offers extensive coverage and peace of mind.

What Is Car Insurance?

Car insurance is a contract between you and an insurance company that protects you financially in case of accidents, theft, or damage involving your car. In exchange for paying a premium (a regular fee), the insurer agrees to cover certain losses or damages as outlined in your policy.

What Is Car Insurance?

Car insurance is a contract between you and an insurance company that provides financial protection against losses related to your vehicle. In exchange for paying a regular premium, the insurer agrees to cover certain damages, theft, or liabilities involving your car.

In Simple Terms:

Car insurance is like a safety net. If your car is damaged in an accident, stolen, or causes harm to others, the insurance company will help pay for the repair costs, replacement, or legal liabilities — depending on the type of policy you choose.

How It Works:

- You buy a policy (usually for a year or more).

- You pay a premium (monthly or yearly fee).

- If an incident occurs (like an accident or theft), you file a claim.

- The insurer evaluates the claim and, if approved, pays for repairs or damages as per the policy.

Common Coverage Includes:

- Damage to your car (accident, fire, natural disaster, etc.)

- Theft of your vehicle

- Injury or damage caused to others (third-party liability)

- Medical expenses for you and passengers (in some policies)

Types of Car Insurance Plans:

- Third-Party Liability Insurance – Covers damage to others (mandatory in most countries).

- Comprehensive Insurance – Covers both third-party and your own car’s damage.

- Add-Ons – Optional extras like zero depreciation, roadside assistance, etc.

Why It Matters:

- It’s often legally required.

- It protects you from huge financial losses.

- It provides peace of mind when you’re on the road.

Why Is Car Insurance Important?

Legal Requirement

In many countries, including India, the U.S., and the UK, car insurance is mandatory by law. At a minimum, drivers are required to have third-party liability insurance, which covers injury or damage to other people and property. Driving without insurance can result in fines, penalties, or even license suspension.

Financial Protection

Accidents can be expensive. Repairing your car, paying for medical treatment, or compensating another party can cost thousands. A car insurance plan helps cover these expenses so you don’t have to pay out of pocket.

Covers Personal Injuries

Good car insurance also includes personal accident coverage. This means the insurer may pay for medical expenses, lost wages, or even death benefits if you’re injured or killed in an accident.

Protection Against Theft or Natural Disasters

Comprehensive car insurance plans protect you if your car is stolen or damaged by fire, floods, storms, riots, or other natural and man-made disasters. This is particularly useful in areas prone to extreme weather.

Third-Party Liability Coverage

If you’re at fault in an accident, you’re liable to pay for the other person’s vehicle damage, injuries, or legal fees. A car insurance plan ensures these costs are covered by the insurer, not you.

Covers Repair Costs

Even minor accidents can lead to expensive repairs. Insurance helps cover the cost of spare parts, labor, and service without draining your savings.

Peace of Mind

Knowing that you’re financially protected if something goes wrong can give you the confidence and peace of mind to drive without constant worry.

No Claim Bonus (NCB) Benefits

If you drive safely and don’t file any claims during a policy year, you’re rewarded with a No Claim Bonus, which can significantly reduce your premium over time.

Add-On Protection

Modern insurance plans offer useful add-ons like:

- Zero Depreciation Cover

- Engine Protection

- Roadside Assistance

These add-ons enhance your overall safety and convenience on the road.

Types of Car Insurance Plans

| Type of Car Insurance Plan | What It Covers | Who Needs It | Pros | Cons |

|---|---|---|---|---|

| Third-Party Liability Insurance | Covers damages or injuries caused to others in an accident you cause. | Drivers who want to meet legal minimum requirements. | Cheapest option; mandatory by law. | Does not cover damage to your own vehicle. |

| Comprehensive Car Insurance | Covers third-party liability + damage to your own vehicle due to accidents, theft, fire, natural disasters. | Most car owners who want broad protection. | Extensive coverage including add-ons. | More expensive premium than third-party. |

| Standalone Add-Ons | Extra coverage like zero depreciation, engine protection, roadside assistance added to basic plans. | Those wanting customized protection. | Tailor your coverage; more protection. | Increases overall premium cost. |

How Does Car Insurance Work?

Car insurance works as a financial agreement between you (the policyholder) and an insurance company. You pay a fixed amount, called a premium, and in return, the insurer agrees to cover certain types of financial losses related to your car — such as accidents, theft, natural disasters, or injuries to others.

Step-by-Step Breakdown of How Car Insurance Works:

Buying a Policy

- You select a car insurance plan based on your needs — either third-party, comprehensive, or customized with add-ons.

- The insurer calculates your premium based on several factors:

- Car type and model

- Location

- Driving history

- Age of the vehicle

- Coverage options

Paying the Premium

- You pay the premium either annually or monthly.

- As long as your policy is active (i.e., premium is paid on time), you’re covered.

An Incident Happens

- This could be an accident, theft, fire, or damage caused by natural disasters.

- Depending on your coverage:

- Third-party insurance pays for damage/injury you cause to others.

- Comprehensive insurance also covers damage to your own car.

Filing a Claim

- You report the incident to your insurer.

- You may need to:

- Submit photos or videos of the damage

- File a First Information Report (FIR) in case of theft or serious accidents

- Provide documents like driving license, registration, and insurance policy

Claim Assessment and Processing

- The insurance company sends a surveyor or assessor to evaluate the damage.

- They check the validity of the claim and estimate repair costs.

Claim Settlement

- Cashless Claim: If you use a network garage, the insurer pays the garage directly.

- Reimbursement Claim: If you use a non-network garage, you pay upfront and get reimbursed later.

- The amount you receive depends on:

- IDV (Insured Declared Value) of your car

- Deductibles (your share of the cost)

- Policy terms and limits

No Claim Bonus (NCB)

- If you don’t file any claims during the policy year, you earn a No Claim Bonus — a discount on your next premium (up to 50% after five claim-free years).

Example:

You have a comprehensive car insurance plan. One day, your parked car is damaged in a hailstorm. You:

- Inform the insurer

- File a claim

- Get the car inspected and repaired at a network garage

- Pay your deductible

- The insurer pays the remaining repair cost directly to the garage

Factors That Affect Your Car Insurance Premium

- Type of coverage (third-party or comprehensive)

- Make and model of your car (expensive cars cost more to insure)

- Your driving history (safe drivers get lower premiums)

- Location (some areas have higher accident rates)

- Add-on covers selected

- Claim history (frequent claims may increase your premium)

Tips for Choosing the Best Car Insurance Plan

Choosing the right car insurance plan is about more than just the lowest premium — it’s about getting the best value, protection, and peace of mind. Here are some smart and practical tips to help you make the best choice:

Understand Your Needs

- New car? A comprehensive car insurance plan is ideal for better protection.

- Old or low-value car? You may only need third-party coverage to meet legal requirements.

- Consider how much you drive, where you park, and how much risk you’re exposed to (traffic, theft, weather, etc.).

Compare Premiums — But Look at Coverage Too

- Don’t just pick the cheapest plan. Lower premiums often mean less coverage.

- Use online comparison tools to compare plans side by side in terms of:

- Premium

- Inclusions

- Add-ons

- Claim process

Check the Claim Settlement Ratio (CSR)

- CSR shows how many claims an insurer has successfully paid.

- Choose insurers with a high CSR (90% or more) to increase your chances of a smooth claim experience.

Look for a Wide Network of Cashless Garages

- A larger cashless garage network ensures you can repair your car without upfront payment.

- Check whether garages near your home or work are in-network.

Choose Useful Add-On Covers

- Add-ons boost the value of your car insurance plan.

- Zero Depreciation: Full claim without depreciation cuts.

- Engine Protection: Covers damage from flooding or oil leaks.

- Roadside Assistance: For breakdowns, flat tires, etc.

- Return to Invoice: Full value reimbursement if your car is stolen or totaled.

- Pick only the add-ons you genuinely need to avoid overpaying.

Know Your Car’s IDV (Insured Declared Value)

- IDV is the maximum amount you’ll get if your car is stolen or totaled.

- A higher IDV means better protection, but a slightly higher premium.

- Don’t go too low just to save money — it could hurt your claim amount later.

Understand the Deductibles

- A deductible is the amount you pay out-of-pocket before insurance kicks in.

- Higher deductibles mean lower premiums, but more expense during claims.

- Choose a balance between premium affordability and claim comfort.

Read the Fine Print

- Always read the policy document carefully.

- Understand:

- What is covered and excluded

- Claim procedures

- Renewal terms

- Penalties for late payments

Check Renewal and Portability Options

- See how easy it is to renew your plan online.

- Some insurers allow you to switch plans or transfer No Claim Bonus (NCB) to a new insurer.

Review Customer Support and App Services

- A good insurer should have:

- 24/7 customer support

- Easy mobile app or web access to claims and policy details

- Fast, transparent claim settlement

Use Reputable Comparison Portals

- Use trusted insurance aggregators (like Policybazaar, Coverfox, or Turtlemint in India) to compare and buy.

- You can apply filters and get real-time quotes with add-ons.

Final Thought:

The best car insurance plan isn’t always the cheapest — it’s the one that gives you the right balance of price, coverage, and service. Taking time to compare and understand your options can save you money and trouble in the long run.

Key Factors to Consider When Evaluating Car Insurance Plans

To determine which car insurance plan offers the most value, consider the following factors:

1. Claim Settlement Ratio (CSR)

The CSR indicates the percentage of claims an insurer settles out of the total claims received. A higher CSR suggests that the insurer is more reliable in settling claims. For instance, SBI General Insurance boasts a CSR of 100%, indicating prompt and efficient claim settlements .

2. Network of Cashless Garages

An extensive network of cashless garages ensures that you can get your vehicle repaired without upfront payments. Insurers like Reliance General Insurance have a vast network of over 8,000 cashless garages across India, making it convenient for policyholders .

3. Add-On Covers

Add-on covers are additional benefits that enhance the coverage of your car insurance plan. Popular add-ons include:

- Zero Depreciation Cover: Ensures that you receive the full claim amount without deductions for depreciation.

- Engine Protection Cover: Covers damages to the engine due to water ingression or oil leakage.

- Roadside Assistance: Provides services like towing, fuel delivery, and minor repairs in case of breakdowns.

Companies like Bajaj Allianz and ICICI Lombard offer a range of add-on covers to customize your policy according to your needs .

4. No Claim Bonus (NCB)

The NCB is a reward for claim-free years, offering discounts on premiums. Some insurers provide an NCB protector add-on, ensuring that you retain your bonus even after making a claim.

5. Digital Convenience

In today’s digital age, insurers offering online policy purchase, renewal, and claim filing provide added convenience. Mobile apps with telematics can also offer real-time driving insights and usage-based discounts.

Top Car Insurance Plans Offering the Most Value

Based on the factors mentioned above, here are some of the top car insurance plans in India:

1. SBI General Insurance

- Claim Settlement Ratio: 100%

- Network Garages: 16,000+

- Key Features: Comprehensive coverage, No Claim Bonus, add-ons like zero depreciation and engine protection, digital services via mobile app and WhatsApp.

2. Bajaj Allianz General Insurance

- Claim Settlement Ratio: 98.5%

- Network Garages: 4,000+

- Key Features: Comprehensive coverage, add-ons like key replacement and consumable expenses, 24×7 roadside assistance, cashless claim service.

3. ICICI Lombard General Insurance

- Claim Settlement Ratio: 94.84%

- Network Garages: 5,600+

- Key Features: Comprehensive coverage, add-ons like zero depreciation and engine protection, 24×7 roadside assistance, personal accident cover up to ₹15 lakh.

4. HDFC ERGO General Insurance

- Claim Settlement Ratio: 89.48%

- Network Garages: 6,800+

- Key Features: Comprehensive coverage, 12 add-on covers, personal accident cover up to ₹15 lakh, paperless insurance procedure facility.

5. Reliance General Insurance

- Claim Settlement Ratio: 98%

- Network Garages: 8,200+

- Key Features: Comprehensive coverage, add-ons like NCB retention and daily allowance benefit, cashless claim service, digital services via mobile app.

Also Read: Which Car Insurance Plan Offers the Most Value?

Conclusion

Choosing the right car insurance plan is crucial for protecting your vehicle and ensuring financial security in case of unforeseen events. While several insurers offer competitive plans, it’s essential to evaluate them based on factors like Claim Settlement Ratio, network of cashless garages, add-on covers, No Claim Bonus, and digital convenience.

Among the top contenders, SBI General Insurance stands out with its 100% Claim Settlement Ratio and extensive network of over 16,000 garages. Bajaj Allianz and ICICI Lombard also offer comprehensive coverage with a range of add-on options, making them suitable choices for many car owners.

Remember, the best car insurance plan is one that aligns with your specific needs and budget. Always compare different plans, read the fine print, and choose the one that offers the most value for your money.

FAQs

1. What is the Claim Settlement Ratio (CSR), and why is it important?

The CSR indicates the percentage of claims an insurer settles out of the total claims received. A higher CSR suggests that the insurer is more reliable in settling claims.

2. How can I reduce my car insurance premium?

You can reduce your premium by opting for higher deductibles, maintaining a claim-free record to avail No Claim Bonus, and choosing add-ons that suit your needs.

3. What is Zero Depreciation Cover?

Zero Depreciation Cover ensures that you receive the full claim amount without deductions for depreciation, making it beneficial for new cars.

4. Can I transfer my existing car insurance policy to another insurer?

Yes, you can transfer your existing policy to another insurer without losing your No Claim Bonus, provided the policy is transferred before the expiry date.

5. Is it necessary to have Roadside Assistance in my car insurance plan?

While not mandatory, Roadside Assistance can be beneficial in case of breakdowns, offering services like towing, fuel delivery, and minor repairs.

6. What is the difference between Third-Party and Comprehensive Car Insurance?

Third-Party Insurance covers damages to third parties involved in an accident where you’re at fault, while Comprehensive Insurance covers both third-party liabilities and damages to your own vehicle.

7. How can I file a claim with my car insurance provider?

You can file a claim by contacting your insurer’s customer service, visiting their website, or using their mobile app. Most insurers offer a cashless claim facility at network garages.